UAE Bank with No Minimum Balance: Best 2026 Options for Businesses and Expats

Why should your bank penalize you for holding a low balance while you’re working hard to scale a new business? If you’re an expat or an entrepreneur in Dubai, you’ve likely dealt with the frustration of opaque fee structures or application rejections based on your initial capital. Finding a reliable uae bank with no minimum balance shouldn’t feel like an impossible task. We understand that every dirham matters during your first year. Those monthly maintenance charges can quickly drain your budget before your company even finds its footing.

This article shows you how to avoid the ‘fall-below fee’ trap and secure a partner that actually supports your financial journey. You’ll discover the most competitive zero-balance accounts for 2026, including the 4.00% interest FAB iSave and digital-first options like Mbank. We’ll simplify the latest KYC requirements and compare the best institutions for both personal and corporate use. By the end of this guide, you’ll have a clear path to a maintenance-free account that keeps your money where it belongs.

Key Takeaways

- Understand why 2026 has become the year of subscription-based banking and how new regulations make it easier for startups to stay compliant.

- Compare the best uae bank with no minimum balance providers, focusing on digital powerhouses like Wio and the reliability of Mashreq NeoBiz.

- Evaluate the trade-offs between 48-hour digital onboarding and the long-term necessity of traditional branch access for cheque deposits.

- Prepare a foolproof documentation package using our checklist to avoid common application hurdles for both mainland and free zone entities.

- Learn how expert matching can expedite your banking setup, turning the most difficult part of business formation into a straightforward step.

The Rise of Zero-Balance Banking in the UAE: What’s Changed in 2026?

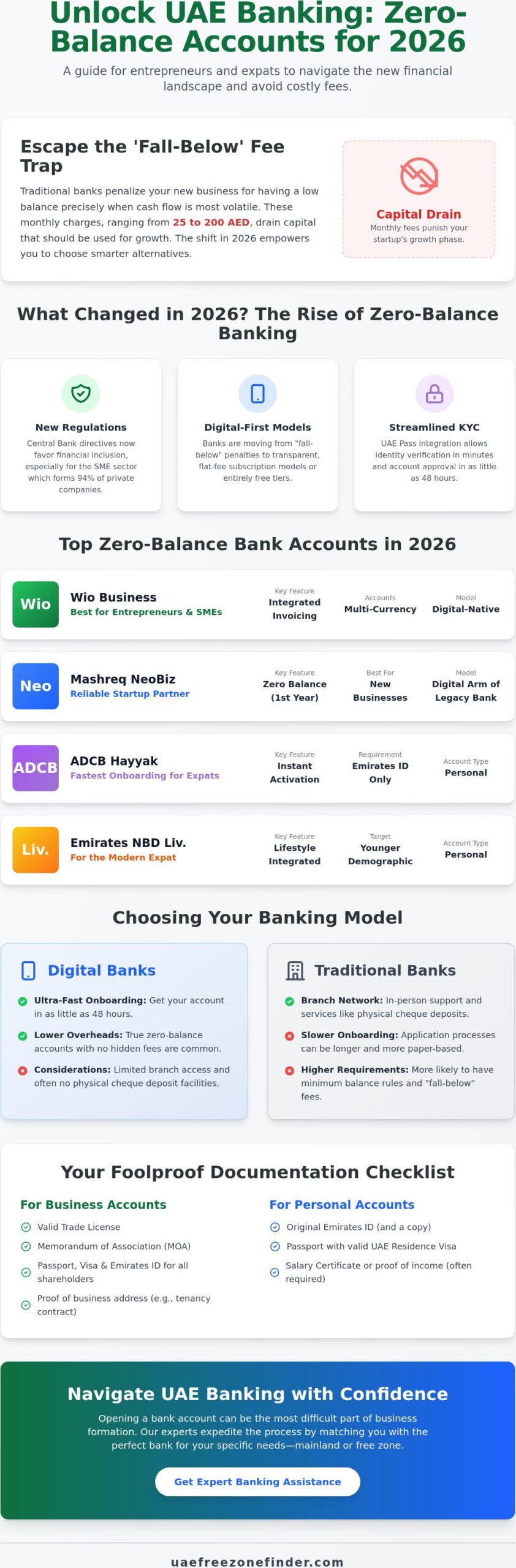

Banking in the Emirates isn’t what it was five years ago. The financial landscape has shifted from a rigid, high-barrier system to one that actively courts the global entrepreneur. By May 2026, the Central Bank of the United Arab Emirates has implemented several directives aimed at financial inclusion, specifically targeting the SME sector that drives over 94% of the country’s private companies. This regulatory push means finding a uae bank with no minimum balance is no longer a desperate search for a loophole; it’s a legitimate strategic choice for your business setup.

The biggest change we’ve seen this year is the move away from the “fall-below” model toward digital-first and subscription-based banking. Instead of punishing you for having low liquidity, many modern banks now offer a flat, transparent monthly fee or even entirely free tiers for basic services. It’s also vital to distinguish between a zero-balance account and a no-maintenance-fee account. A true zero-balance account lets you keep exactly nil in your ledger without penalty. In contrast, some “no-maintenance” options might waive the monthly charge only if you meet specific criteria, like a minimum salary transfer of 5,000 AED or a certain number of monthly transactions.

Streamlined KYC (Know Your Customer) protocols have also transformed the onboarding experience in 2026. Thanks to the integration of the UAE Pass and centralized government databases, the days of carrying thick folders of paper to a branch are largely over. New residents can often verify their identity and residency status through a mobile app in under ten minutes, with account approval following in as little as 48 hours.

Understanding the ‘Fall-Below’ Fee Trap

Traditional banking models often hide a sting in the tail. If your average monthly balance drops even one dirham below the bank’s threshold, you’re hit with a “fall-below” fee. These charges typically range from 25 AED to 200 AED per month depending on the institution. For a startup, these costs are incredibly damaging because they drain capital precisely when cash flow is most volatile. It’s a penalty for being in the growth phase, which is why we always steer our clients toward more flexible, modern alternatives.

Why Minimum Balances Exist (and Why They’re Disappearing)

Banks historically required minimum balances to ensure they had enough liquidity to fund their lending operations. However, digital banks have disrupted this revenue model. Because they don’t have the massive overhead of physical branches or thousands of tellers, they don’t need to force customers into high-balance tiers to remain profitable. Increased competition has forced traditional banks to adapt; they’re now dropping these requirements to prevent a mass exodus of clients to more agile, digital-native competitors.

Top UAE Banks Offering No Minimum Balance Accounts in 2026

Selecting a uae bank with no minimum balance used to mean compromising on features, but 2026 has changed that. Wio Bank has emerged as the dominant digital-first powerhouse, offering a platform that handles both complex corporate needs and personal spending with equal of. For those who value the security of a legacy institution but want a modern interface, Mashreq Neo and NeoBiz remain top-tier choices. If you’re an expat looking for immediate utility, ADCB Hayyak provides one of the fastest onboarding experiences in the market, allowing you to activate an account using only your Emirates ID.

The landscape is now split between digital-native banks and traditional giants that have successfully pivoted. Emirates NBD’s ‘Liv’ continues to capture the younger demographic and new expats with its lifestyle-integrated banking. Meanwhile, specialized players like Mbank and Ruya Bank have entered the fray, offering zero-balance accounts with no hidden fees and the ability to deposit cash at major exchange houses or partner ATM networks. It’s a buyer’s market, and the competition for your deposits has never been more intense.

Best Options for Business Owners and SMEs

Wio Business is arguably the most versatile tool for entrepreneurs today. It supports multi-currency accounts and features integrated invoicing, which is essential when you’re Doing Business in the UAE. Mashreq NeoBiz is another reliable partner, specifically designed for startups that need zero-balance tiers during their first year of operation. These digital platforms are particularly attractive because they often waive the requirement for a physical office lease, a common hurdle for those using virtual office setups. If you’re unsure which bank aligns with your specific trade license, our team can help with expert matching to streamline your application.

Best Options for Personal Savings and Expats

If your goal is to grow your wealth while maintaining liquidity, the FAB iSave account is a standout. It currently offers a competitive 4.00% interest rate on new funds deposited through June 30, 2026, with no minimum balance required. HSBC’s E-Saver is another strong contender for those who want a global name, offering tiered interest rates that start at 0.25% for balances under 100,000 AED. For expats from India or Pakistan, the Sharjah Islamic Bank (SIB) Digital account is highly recommended, as it provides free money transfers to those corridors and requires a minimum salary of only 1,000 AED. While older products like the ADIB Smart account are no longer available for new users, these 2026 options offer better technology and higher returns.

Digital vs. Traditional: Choosing the Right Banking Model

Deciding between a digital disruptor and a traditional legacy bank often depends on your specific operational needs. While almost everyone wants a uae bank with no minimum balance to keep costs low, the choice of infrastructure can make or break your daily workflow. Digital-only platforms have fundamentally changed expectations around speed. Today, it’s standard for digital banks to approve new accounts within 48 hours. This efficiency is a lifeline for new startups that can’t afford to wait weeks for a traditional institution to process a mountain of paperwork.

Traditional banks still hold the upper hand in physical logistics. If your business handles significant cash or requires the issuance of physical cheques for rent and supplier payments, a brick-and-mortar branch is essential. While digital players like Ruya Bank allow cash deposits through exchange house networks, it’s not always as simple as using a bank’s own dedicated CDM (Cash Deposit Machine). Additionally, traditional institutions often provide a human relationship manager. This person acts as a bridge during complex transactions, something an AI-powered chat interface can’t always match.

Currency exchange is where the competition gets fierce. Digital banks usually provide mid-market rates and transparent remittance fees, which is a major win for expats and global traders. Traditional banks might have higher margins on exchange rates, but they offer the stability of a physical presence and a long history in the region. You’re essentially choosing between the agility of the future and the established security of the past.

When to Go Digital-First

The digital-first path is perfect for freelancers and e-commerce entrepreneurs who live on their devices. These accounts offer lower monthly costs and often sync directly with your accounting platforms. Managing your finances, from VAT filings to payroll, becomes a task you can handle in minutes from your phone. It’s the most efficient way to maintain a uae bank with no minimum balance without sacrificing modern technological features.

When a Traditional Bank Still Makes Sense

Legacy banks are still the right choice if you’re eyeing long-term credit facilities or corporate mortgages. They’re also vital if your business model relies on physical cheques, which remain common for commercial leases in many Emirates. Having a physical branch to visit provides a sense of security that many international investors still prefer. If your company needs high-level trade finance or complex letter-of-credit services, the traditional model remains the industry standard for a reason.

Crucial Requirements for Opening Your UAE Bank Account

Paperwork is the gatekeeper of your financial freedom in the Emirates. Even if you’ve identified the ideal uae bank with no minimum balance, your application’s success hinges on the precision of your documentation. Banks in 2026 are under strict federal mandates to verify every detail of an applicant’s profile. For individuals, this starts with a valid passport, a residency visa, and the physical Emirates ID. For corporate entities, the list is more extensive, requiring a valid trade license, the Memorandum of Association (MoA), and often a proof of address like an Ejari or utility bill.

Don’t overlook the role of the Al Etihad Credit Bureau (AECB). Your personal credit history is now a standard part of the vetting process for both personal and business accounts. A history of bounced cheques or unpaid liabilities in your home country or the UAE can lead to an immediate rejection. Banks use this data to assess the risk of maintaining your account, even when you aren’t seeking credit. If you’re concerned about your eligibility, you can consult with our experts to review your profile before submitting an application.

The 2026 KYC Checklist for Business Owners

Know Your Customer (KYC) procedures have become more narrative-driven. You must provide a clear description of your business activities and a detailed “source of funds” statement. Banks want to know exactly how your capital was earned and who the Ultimate Beneficial Owners (UBO) are. If any individual owns more than 25% of the company, their personal documents must be included. A common reason for rejection is a mismatch between the declared business activity on the trade license and the actual transactions expected in the account. Be prepared to provide invoices or contracts from potential clients to prove your business is operational.

Opening an Account Before Your Emirates ID Arrives

Waiting for your physical Emirates ID can take several weeks, but you don’t always have to wait to start banking. Some institutions offer “non-resident” or “investor” accounts that can be opened with just a passport and a copy of your entry permit. However, these accounts come with significant limitations. They often lack a chequebook facility and may actually require a minimum balance until your residency is fully processed. Once your visa is stamped and your ID arrives, you can transition to a full resident account. This move typically unlocks the zero-balance features and provides access to more robust digital banking tools without the usual administrative friction.

Expert Assistance: Bridging the Gap Between Setup and Banking

Many entrepreneurs discover that obtaining a trade license is the easiest part of their journey. The real challenge begins when trying to open a corporate account. In 2026, banks have become significantly more selective about their clients, often leading to high rejection rates for those who approach the process without a clear strategy. At UAE Free Zone Finder, we act as the bridge between your corporate structure and the financial institutions you need to thrive. We understand that finding a uae bank with no minimum balance is a top priority for lean startups, and we ensure your application doesn’t get buried in the compliance pile.

Our approach is based on transparency and pre-emptive vetting. We partner with top-tier banks to understand their current risk appetite for specific jurisdictions and business activities. This allows us to guide you toward the institutions most likely to approve your specific profile. Our PRO services aren’t just about filing papers; they’re about ensuring your business is positioned as a low-risk, high-value client from the very first meeting. We’ve seen that 85% of application delays are caused by simple documentation errors that could’ve been caught before submission.

How We Simplify the Process

We start by matching your specific license type with the right banking partner. Not every bank is a fan of every free zone, and some institutions are more comfortable with certain trading or service activities than others. We review your entire documentation package before it ever reaches a bank officer’s desk. This includes checking for Ultimate Beneficial Owner (UBO) clarity and ensuring your business activity descriptions align with bank-friendly terminology. Beyond the initial setup, we provide ongoing support to help you stay compliant with VAT and corporate tax regulations, which are critical for maintaining a healthy relationship with your chosen uae bank with no minimum balance.

Ready to Start Your UAE Business Journey?

There’s a powerful synergy between choosing the right free zone and securing a bank account. Waiting until your company is already formed to think about banking is a common mistake that can lead to months of operational delays. You need a partner who understands the shortcuts and the pitfalls of the UAE’s bureaucratic system. We provide the steady hand you need to navigate these regulatory waters with confidence. If you’re ready to secure your financial future in the Emirates, we’re here to make the impossible feel attainable through step-by-step guidance. Get expert assistance with your UAE corporate bank account today and let us handle the complexities while you focus on growth.

Secure Your Financial Future in the Emirates

Choosing a uae bank with no minimum balance is no longer about settling for less. It’s about finding a strategic partner that respects your capital. In 2026, the shift toward digital-first banking has removed the burden of high maintenance fees, but the complexity of KYC remains a significant barrier for many. By aligning your business setup with the right banking institution from the start, you avoid the operational delays that stall so many new ventures.

As a strategic partner of UAE Free Zone Finder with deep expertise in 40+ UAE Free Zones, we specialize in removing these bureaucratic hurdles. Our dedicated banking assistance for international investors ensures that your application is optimized for approval. You don’t have to navigate this landscape alone. We provide the insider knowledge needed to match your license with the perfect financial institution. Start your UAE business and banking journey today and take the first step toward a hassle-free corporate life. The Emirates is ready for your vision, and we’re ready to help you build it.

Frequently Asked Questions

Can I open a UAE bank account with zero balance as a non-resident?

Yes, you can open a non-resident account with zero balance, but these typically come with limitations like the absence of a chequebook and higher compliance scrutiny. Banks such as FAB and ADCB offer these options to international investors who haven’t yet received their residency. You’ll likely need to transition to a full resident account once your Emirates ID is issued to access more robust digital features.

Which bank is best for a small business in the UAE with no minimum balance?

Wio Business is currently the most versatile choice for a uae bank with no minimum balance due to its 48-hour onboarding and integrated invoicing tools. Mashreq NeoBiz is a strong runner-up, specifically for its tiered approach that caters to startups in their first year. Choosing the right one depends on whether you prefer a pure digital experience or a hybrid model with occasional branch access.

What is a ‘fall-below fee’ and how much does it cost?

A fall-below fee is a monthly penalty charged when your average balance drops below the bank’s required threshold. In 2026, these charges typically range from 25 AED to 200 AED depending on the institution. Selecting a zero-balance account eliminates this risk entirely, protecting your cash flow during the volatile early stages of business growth or during months with high personal expenses.

Do I need a physical office to open a business bank account in the UAE?

No, a physical office isn’t strictly required if you use digital-first banks like Wio or NeoBiz. These platforms accept virtual office addresses or flexi-desks common in many free zones across the Emirates. However, traditional banks might still request a physical Ejari for certain corporate account tiers, so it’s vital to match your office setup with your banking choice before applying.

How long does it take to open a zero-balance bank account in 2026?

Digital banks typically approve accounts within 48 hours if your documentation is perfect and your UAE Pass is active. Traditional institutions usually take between two and four weeks due to their manual compliance checks and physical meeting requirements. Using the UAE Pass for digital verification has reduced the average processing time for residents by of compared to previous years.

Are digital banks like Wio and Mashreq NeoBiz safe for large transactions?

Yes, these banks are fully regulated by the Central Bank of the UAE and follow the same security protocols as legacy institutions. They use advanced encryption and multi-factor authentication to secure large corporate transfers. Their digital nature doesn’t mean they’re less secure; it simply means they have more efficient infrastructure for managing high-volume transactions without the overhead of physical branches.

Can I get a credit card with a zero-balance bank account?

Yes, you can obtain a credit card, but the approval is based on your monthly income or a fixed deposit rather than your current account balance. For expats, a minimum salary of 5,000 AED is a common requirement for most basic cards in 2026. Some banks also offer “secured” credit cards where the limit is backed by a specific amount held in a separate savings pot.

What happens if I don’t use my zero-balance account for several months?

Your account will be marked as “dormant” if there’s no transaction for six consecutive months. Once dormant, you won’t be able to make transfers or use your debit card until you visit a branch or use the bank’s app to re-verify your identity. It’s best to perform at least one small transaction every quarter to keep the account active and avoid the reactivation process.

Disclaimer

The information provided in this article is intended for general informational purposes only and reflects conditions as understood at the time of publication. Free zone regulations, fees, and requirements in the UAE are subject to change. Readers are advised to verify details with the relevant free zone authority or regulatory body before making any business decisions. For personalised guidance, our business setup experts at UAE Free Zone Finder are available to assist — contact us at info@uaefreezonefinder.com or call +971-507864823.