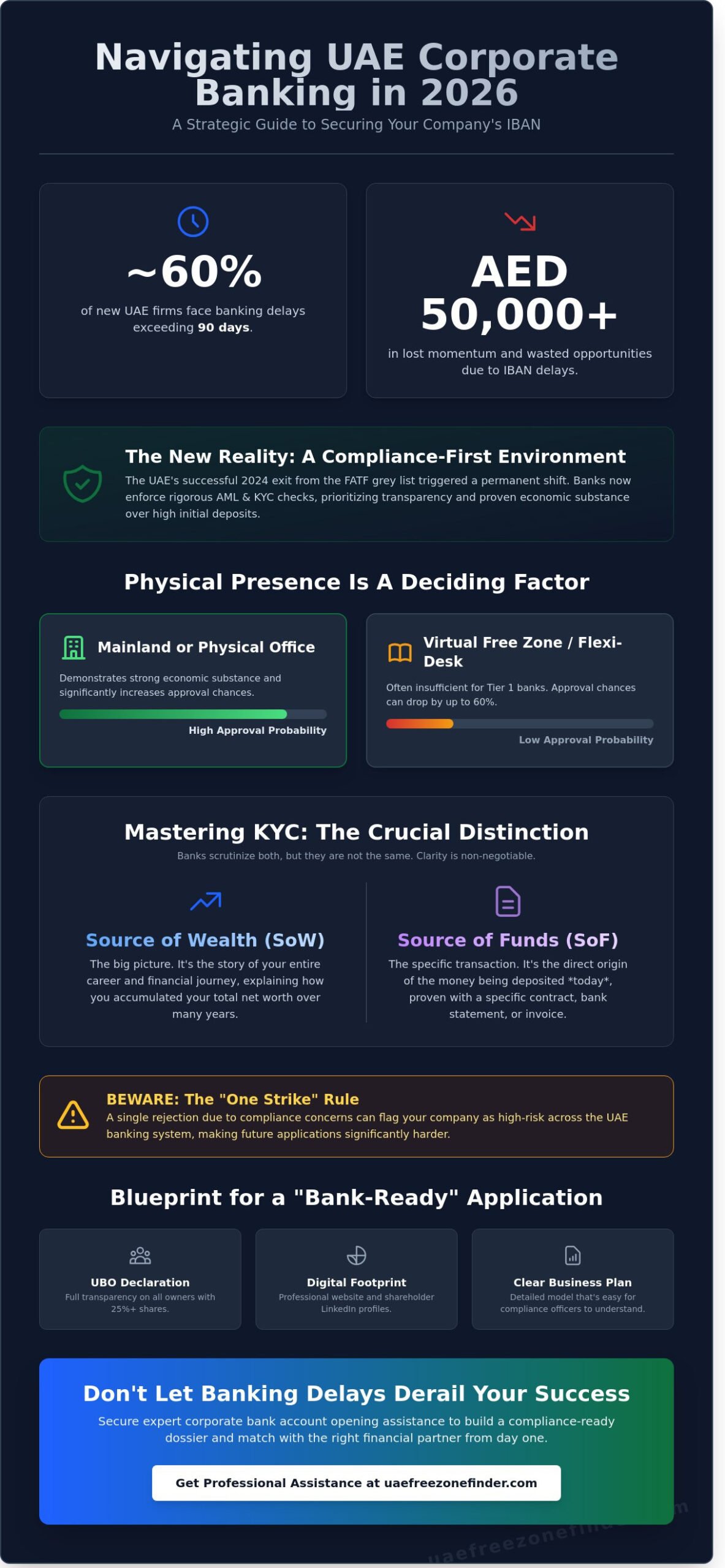

Did you know that nearly 60% of new UAE firms face banking delays exceeding 90 days according to recent market observations? You’ve likely felt the sting of providing mountains of paperwork only to receive a generic rejection letter weeks later. It’s exhausting to have your capital ready while your operations remain frozen because of an IBAN delay. We recognize that the 2026 regulatory environment has made the process feel like a maze with no exit.

This strategic guide provides the professional corporate bank account opening assistance you need to secure a reliable financial partner. You’ll master the complexities of modern compliance and learn how to position your company as a low-risk, high-value client. We’ll walk through the current Central Bank of the UAE requirements, essential documentation for non-residents, and the specific criteria banks use to evaluate your industry today.

Key Takeaways

- Navigate the 2026 banking landscape by uncovering the hidden compliance hurdles and transparency requirements that often lead to unexpected application rejections.

- Master the nuances of modern KYC protocols, including the critical distinction between your source of wealth and your source of funds to satisfy bank underwriters.

- Identify whether a traditional “Big 3” local bank or a specialized UAE neobank is the right fit for your business activity and minimum balance capabilities.

- Secure expert corporate bank account opening assistance to build a “compliance-ready” dossier that presents your business narrative effectively to financial institutions.

- Follow a strategic blueprint to match your firm with the ideal banking partner, ensuring you don’t just get approved but stay compliant for the long term.

The Reality of UAE Corporate Banking in 2026: A Strategic Hurdle

Establishing a business in the UAE used to be the hard part, while banking was an afterthought. That script flipped entirely by early 2026. Today, securing a functional IBAN is the single most significant hurdle for international investors. The UAE’s successful exit from the FATF grey list in 2024 triggered a permanent shift toward extreme transparency. Banks now scrutinize every detail of your business model before they even look at your initial deposit. It’s no longer about whether you have the capital; it’s about whether your company fits a very narrow risk profile.

The cost of waiting is steep. A delay of 90 days in opening an account can cost a startup upwards of AED 50,000 in lost operational momentum and wasted trade opportunities. If you can’t pay your employees or settle invoices with suppliers, your market entry stalls before it begins. This is why seeking corporate bank account opening assistance isn’t just a luxury, it’s a tactical necessity for anyone serious about doing business in the region.

The Compliance-First Environment

The Central Bank of the UAE (CBUAE) now mandates rigorous Anti-Money Laundering (AML) and “Know Your Customer” (KYC) checks that rival those in London or New York. By 2026, regulations require every business to prove “Economic Substance.” This means you need more than just a trade license. Banks want to see a physical presence, such as a leased office or local employees. When you look at the List of banks in the United Arab Emirates, you’ll see a mix of local giants and international branches. Each has its own risk appetite, but they all share a common fear of regulatory fines. If your company is in a “virtual” Free Zone without a physical office, your chances of approval can drop by 60% compared to Mainland entities.

Why Professional Assistance Is No Longer Optional

- Jurisdiction Matters: Mainland companies often find more doors open than Free Zone entities.

- Hidden Rejections: Banks rarely give a reason for a “no,” but it’s usually tied to your source of wealth or unclear business activity.

- Physical Presence: A flexi-desk is no longer enough for most Tier 1 banks in 2026.

- Expert Matching: Not every bank wants every business. Finding the right fit is 80% of the battle.

Efficiency is the hallmark of a successful UAE launch. You don’t have time to guess which bank will accept your specific nationality or industry. You need a steady hand to guide you through the bureaucratic maze. We provide the clarity and strategic direction required to turn a complex administrative requirement into a clear, actionable resolution. Don’t let a bank’s compliance department be the reason your vision for the UAE fails to launch.

What Banks Really Want: The KYC and AML Checklist

Banks in the UAE don’t just want your business; they want to ensure you aren’t a liability. They operate under strict KYC and AML regulations to maintain the country’s standing in the global financial market. You’ll need to provide full transparency regarding the Ultimate Beneficial Owner (UBO). If you own 25% or more of the shares, your entire financial history is essentially an open book for the bank’s compliance team.

Standard documentation is the baseline. This includes your Trade License, Memorandum of Association (MOA), and your Emirates ID. However, the bank’s “Know Your Customer” process goes much deeper than paperwork. They’ll look at your digital footprint. A professional website and a clear LinkedIn profile for shareholders aren’t just for marketing; they’re proof of existence. If a bank can’t find your professional history online, they may flag the company as a high-risk shell entity.

One major hurdle is the distinction between Source of Wealth and Source of Funds. Your Source of Wealth is the story of your career; it’s how you built your net worth over the last 10 or 20 years. Source of Funds is the specific origin of the money you’re transferring today. If you’re transferring د.إ250,000 for your initial deposit, you must show the exact bank statement, dividend note, or property sale contract that generated that specific sum. Clarity here is the difference between an approval and a month-long delay.

Proving Your Business Legitimacy

Your business plan shouldn’t be a marketing brochure. It needs to be a risk assessment document that speaks the language of a banker. Show your expected transaction volumes clearly. If you’re forecasting د.إ500,000 in monthly turnover, back it up with a list of your top three suppliers and customers. Providing a reference letter from a reputable bank outside the UAE where you’ve held an account for at least 24 months adds immediate credibility. If you’re struggling to organize these details, professional corporate bank account opening assistance can help you present a profile that meets local compliance standards on the first attempt.

Personal Requirements for Shareholders

While not every shareholder needs a UAE residency visa, having at least one resident director simplifies the process significantly. Your home country’s tax residency also plays a role. If you’re a tax resident in a jurisdiction that doesn’t share financial data, expect 40% more scrutiny. During the physical interview, stay focused. Keep your answers strictly aligned with the activities listed on your Trade License. Don’t mention speculative future projects or high-risk industries like unregulated commodities if they aren’t on your license, as this often leads to an immediate file closure.

Traditional vs. Digital Banks: Finding Your Perfect Fit

Choosing where to park your capital is a strategic decision that dictates your operational tempo. In the UAE, the banking sector has split into two distinct paths: the “Big 3” local giants and the agile neobanks. Emirates NBD, First Abu Dhabi Bank (FAB), and Abu Dhabi Commercial Bank (ADCB) dominate the traditional landscape. These institutions offer the highest levels of prestige and a full suite of corporate products. However, they demand commitment. You should expect minimum average balance requirements to start at AED 50,000, often climbing to AED 200,000 for premium corporate tiers. Onboarding at these legacy banks can take anywhere from four to twelve weeks due to intensive KYC protocols. This is why many entrepreneurs seek corporate bank account opening assistance to navigate the documentation hurdles and avoid application rejections.

International banks like HSBC, Standard Chartered, and Citibank provide a different value proposition. They’re the best fit for manufacturing firms or global trading houses that require multi-currency accounts and seamless cross-border transfers. If your business model involves importing raw materials from Europe and selling to Asian markets, the global network of an international bank is indispensable. Conversely, if you’re launching a lean E-commerce site or a consultancy, UAE neobanks like Wio or Mashreq NeoBiz are often more appropriate. These digital-first platforms prioritize speed, frequently issuing an IBAN in as little as 48 hours. While they lack the deep credit facilities of traditional banks, their interface and ease of use are unmatched for daily operations.

When to Choose a Traditional Bank

Traditional banks are essential for high-volume businesses that require a human touch. If your company needs trade finance, Letters of Credit, or physical cheque books for commercial rent, a legacy institution is your only viable option. You’ll benefit from a dedicated relationship manager who understands the specific regulatory nuances of your jurisdiction. For high-net-worth corporate entities, the stability and long-term reputation of a “Big 3” bank provide a level of credibility that digital platforms can’t yet replicate. They’re built for complex, heavy-duty financial engineering.

The Digital Alternative for SMEs and Startups

For early-stage entrepreneurs, digital banks remove the high barrier to entry. Many neobanks offer zero or low minimum balance accounts, which is a lifesaver when you’re managing tight startup capital. The onboarding process is entirely app-based, allowing you to bypass physical branch visits. These platforms are designed for the modern era; they integrate directly with accounting software and offer automated VAT filing tools. Utilizing corporate bank account opening assistance for a digital setup ensures you choose a platform that scales with your revenue without hitting unexpected transaction limits.

A Step-by-Step Blueprint for a Successful Application

Opening a corporate account in the UAE isn’t a simple administrative task; it’s a rigorous vetting process. Banks here operate under strict Central Bank of the UAE (CBUAE) guidelines to prevent money laundering and ensure financial stability. You’ll find that getting professional corporate bank account opening assistance is often the difference between a three-week approval and a six-month rejection cycle. Success requires a methodical approach that starts long before you walk into a branch.

First, you must select the right bank. Not every institution has an appetite for every industry. For example, a bank that favors local mainland trading companies might hesitate to onboard a high-tech startup based in a Northern Emirate freezone. You need to match your business activity and projected annual turnover with the bank’s specific risk profile. Once you’ve identified a target, you’ll prepare a compliance-ready dossier. This includes your trade license, Memorandum of Association (MOA), and shareholder CVs. All documents from outside the UAE require full attestation by the Ministry of Foreign Affairs (MOFA), a step many entrepreneurs overlook.

- Pre-evaluation: Don’t submit a formal application immediately. Send a summary of your profile to a relationship manager to gauge their interest. This saves your company from having a “rejected” status on record.

- The KYC Interview: Whether it’s a face-to-face meeting or a digital verification via a secure app, you’ll need to explain your business model clearly. You should be ready to discuss your primary suppliers and customers.

- Ongoing Compliance: Your job isn’t finished once the IBAN is issued. Banks conduct annual reviews. If your transaction patterns shift significantly from your initial profile, they’ll freeze the account until you provide supporting invoices.

Aligning with 2026 Tax Regulations

The UAE’s financial landscape changed forever with the introduction of the 9% corporate tax on profits exceeding AED 375,000. By 2026, every business will be expected to show a mature tax history. Completing your corporate tax registration is now a prerequisite for maintaining a healthy bank standing. Banks are increasingly asking for tax registration numbers (TRN) during annual reviews. If your VAT filings don’t align with the turnover shown on your bank statements, it triggers an internal red flag. Professional bookkeeping isn’t just for the tax man; it’s for your banker too.

Managing the Post-Approval Phase

Once you receive your approval, activate your online banking immediately. Set up multi-factor authentication (MFA) using a UAE-linked mobile number to ensure you don’t get locked out while traveling. You’ll likely start with specific daily transaction limits, often around AED 50,000 to AED 100,000 for new SMEs. If you need to send funds to jurisdictions that are under increased monitoring by the FATF, expect your banker to ask for the underlying contract before they release the payment. Building a rapport with your dedicated manager from day one ensures these hurdles don’t stop your operations. Utilizing corporate bank account opening assistance helps you set these expectations early so there are no surprises.

Ready to secure your company’s financial future in the Emirates? Get expert matching for your corporate bank account today.

How UAE Free Zone Finder Streamlines Your Banking Journey

Opening a corporate account in the Emirates often feels like the most challenging part of starting a business. It shouldn’t be. At UAE Free Zone Finder, we act as the bridge between your entrepreneurial vision and the UAE’s strict regulatory frameworks. Our corporate bank account opening assistance is designed to remove the guesswork, ensuring you don’t waste months waiting for a rejection letter that offers no explanation.

We operate as your expert matchmaker. Not every bank has an appetite for every industry. A bank that loves e-commerce might avoid physical commodity trading; a bank that caters to local startups might struggle with complex international holding structures. We pair your specific business profile with the right banking partner from day one. This targeted approach prevents the “scattergun” method that often leads to internal blacklisting at major financial institutions.

Our team doesn’t just collect your passport copies. We build a narrative. Banks reject files because they don’t understand the business model or the source of wealth. We curate your documentation to answer compliance questions before they’re even asked. By providing direct access to senior relationship managers, we help you bypass generic call centers and automated emails. Our support is truly end-to-end; we stay by your side from the initial free zone company formation until your first deposit is successfully cleared.

Our Proven Methodology

We’ve developed a rigorous pre-screening process that identifies potential red flags in your application within 48 hours. This step alone saves our clients an average of eight to twelve weeks of wasted time. We handle the technical back-and-forth with bank compliance teams, speaking their language so you don’t have to. Our track record includes securing approvals for businesses in sectors often labeled as high-risk, such as crypto-assets and international logistics, where we’ve maintained a success rate significantly higher than the industry average.

Beyond the Bank Account

A bank account isn’t an isolated tool; it’s the heart of your local operations. We ensure your banking setup integrates perfectly with your residency visas and VAT compliance requirements. For instance, we help you monitor the AED 375,000 mandatory VAT registration threshold to ensure your account remains in good standing with the Federal Tax Authority.

- Coordination of Emirates ID biometrics to speed up account activation.

- Advice on maintaining the minimum average balance to avoid monthly penalties.

- Ongoing support for trade license renewals to prevent account freezes.

Don’t leave your financial foundation to chance. If you’re ready to secure a stable banking partner for your UAE enterprise, book a consultation with us today. We’ll build a banking strategy that supports your growth from the first dirham to your global expansion.

Future-Proof Your UAE Business Banking

Navigating the financial landscape in 2026 demands more than just a stack of documents. It requires a deep understanding of the Central Bank of the UAE’s latest AML regulations and a clear strategy for choosing between traditional giants and agile digital platforms. You’ve learned that preparation is the only way to avoid the common pitfalls that often delay new business accounts for months. Success hinges on precise KYC documentation and selecting a bank that aligns with your specific trade volume and jurisdiction.

We’ve built direct partnerships with major UAE banks to ensure your application doesn’t get stuck in a bureaucratic queue. Our expert compliance team handles the heavy lifting of KYC and AML hurdles, providing the corporate bank account opening assistance you need to stay focused on growth. We offer integrated support that covers everything from your initial company setup and residency visas to final bank approval. You don’t have to face these complex regulatory hurdles alone when you have a partner who knows the system inside out.

Get Expert Assistance for Your UAE Corporate Bank Account Opening

Your vision for expansion deserves a banking partner that works as hard as you do. Let’s get your corporate account active and ready for business today.

Frequently Asked Questions

Can I open a corporate bank account in the UAE without being a resident?

Yes, you can open a corporate bank account as a non-resident, though the process is significantly more rigorous than for residents. UAE banks classify non-resident accounts as high-risk under Central Bank compliance regulations, which often means you’ll need to maintain a higher minimum average balance, often starting at AED 200,000. You’ll also need to provide comprehensive proof of your business activities and personal bank statements from your home country to satisfy strict KYC protocols.

What is the average time it takes to open a business bank account in 2026?

The timeline for opening a business bank account in 2026 typically ranges between 4 and 12 weeks depending on your company’s risk profile. While digital-first banks have streamlined their initial review to roughly 10 working days, traditional commercial banks still require about 60 days for full compliance vetting. Utilizing professional corporate bank account opening assistance can often reduce this period by ensuring your documentation is perfect before the first submission.

Are there UAE banks with no minimum balance requirements for startups?

Several digital banking platforms like Wio and Mashreq NeoBiz offer specialized accounts for startups that feature zero minimum balance requirements for an introductory period. After this initial phase, you’ll usually need to maintain a modest balance of AED 3,000 to AED 5,000 to avoid monthly service fees. These digital options are excellent for new entrepreneurs who don’t want to lock up the AED 50,000 or more typically required by tier-one traditional banks.

Why do UAE banks ask for a personal bank statement from my home country?

Banks request these statements to verify your “Source of Wealth” and comply with global Anti-Money Laundering (AML) standards. They generally look for a consistent history of at least 6 months to ensure the capital you’re using to fund your UAE venture is legitimate. If your home country statements show irregular large deposits without clear origins, the bank’s compliance department will likely flag your application for additional scrutiny.

Can a Free Zone company open a bank account with a mainland bank?

A Free Zone company can absolutely open an account with a mainland bank, and many entrepreneurs prefer this route for the better international services offered. Most major institutions like Emirates NBD or ADCB welcome Free Zone clients, provided the business activity aligns with their internal risk appetite. You just need to ensure your Free Zone license is valid and that you can demonstrate a clear business link to the UAE market if requested.

What happens if my corporate bank account application is rejected?

If your application is rejected, the bank isn’t legally required to give you a specific reason, but they’ll usually cite internal policy or compliance risk. It’s best to wait at least 30 days before applying to the same institution again, as your details will remain in their internal tracking system. Your most effective move is to pivot to a different bank or seek corporate bank account opening assistance to identify and resolve the specific red flags that caused the initial rejection.

Do I need a physical office to open a business bank account in the UAE?

Most traditional UAE banks require a physical office lease, such as an Ejari or a certified warehouse agreement, to approve a corporate account. While many Free Zones offer “Flexi-desk” or “Virtual Office” solutions, these often lead to delays or rejections with major banks that view a physical footprint as a sign of operational substance. If you only have a virtual desk, you’ll likely be limited to digital neobanks that have more flexible requirements regarding physical workspace.

Is it possible to open a UAE corporate bank account remotely?

You can’t complete the entire process remotely because UAE Central Bank regulations require the physical presence of the company’s ultimate beneficial owner for identity verification. While you can submit 95% of your application online from abroad, you’ll eventually need to visit the UAE for at least one day to sign the final bank forms and provide original passport signatures. Some digital banks allow for verification via the UAE PASS app, but this still requires you to have a valid Emirates ID and residency.

Disclaimer

The information provided in this article is intended for general informational purposes only and reflects conditions as understood at the time of publication. Free zone regulations, fees, and requirements in the UAE are subject to change. Readers are advised to verify details with the relevant free zone authority or regulatory body before making any business decisions. For personalised guidance, our business setup experts at UAE Free Zone Finder are available to assist — contact us at info@uaefreezonefinder.com or call +971-507864823.