UAE Business Bank Account Requirements for Non-Residents: The 2026 Checklist

Your non-resident status isn’t the primary reason your bank application failed; it’s often a lack of proof that your business has a legitimate “reason to exist” within the UAE’s $500 billion economy. Most entrepreneurs assume a trade license is a golden ticket, yet they’re frequently met with complex KYC hurdles and minimum balance demands that can reach AED 200,000 at traditional institutions. Mastering the specific uae business bank account requirements for non-residents is the only way to bypass these gatekeepers and secure your company’s financial future in 2026.

We understand how frustrating it’s to face total silence from banks while your capital sits idle. It’s a common hurdle for international founders, but it’s one we’ve successfully navigated for thousands of investors. This guide provides a definitive checklist of mandatory documents, explains the 9% corporate tax implications for non-resident entities, and identifies digital-first banks like Wio or RAKstarter that are actively welcoming global business owners. You’ll gain a clear, step-by-step roadmap to satisfy compliance officers and get your account active without the typical six-month processing delay.

Key Takeaways

- Learn why banks categorize international owners as “high-risk” and how you’ll present your business case to overcome these initial compliance hurdles.

- Access the definitive 2026 checklist for uae business bank account requirements for non-residents, covering everything from MOAs to mandatory entry stamps.

- Discover the importance of the “soft review” process, a critical step that lets you gauge a bank’s interest before you’ve filed a formal application.

- Identify which personal financial records are non-negotiable for shareholders, ensuring your home-country documentation meets strict UAE regulatory standards.

- See how professional pre-screening helps you bypass common rejection triggers that’ll otherwise stall your application for months.

Why Non-Resident Business Banking in the UAE is Different

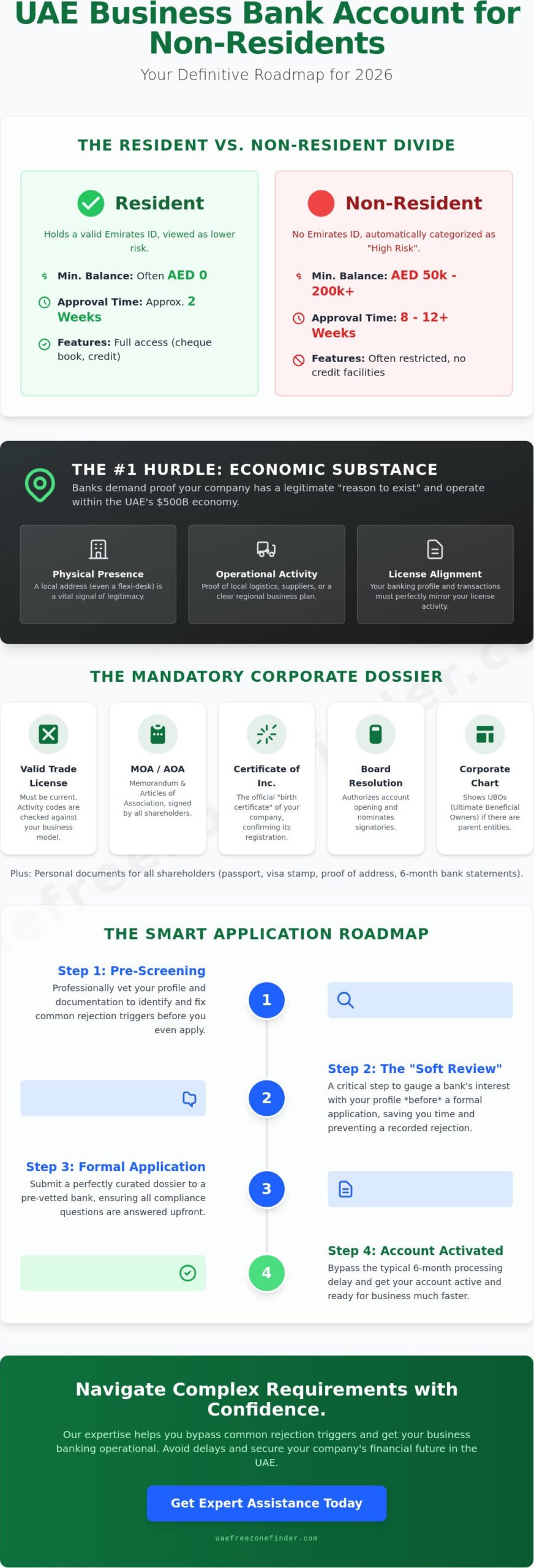

In the eyes of a UAE compliance officer, you’re a non-resident the moment you apply for an account without a valid Emirates ID. It doesn’t matter if you’ve visited Dubai twenty times or own property in the Marina; without that residency card, you fall into a specific risk category. This distinction is the core reason why uae business bank account requirements for non-residents are significantly more stringent than for local residents. Banks view international owners through a lens of ‘high-risk’ because they can’t easily track your global financial footprint or verify your physical presence within the country.

By early 2026, regulatory pressure from the Central Bank of the UAE has intensified. There’s a massive push toward transparency, specifically regarding Ultimate Beneficial Ownership (UBO). If you’re running a business from London or Mumbai, the bank needs to be 100% certain about where your capital originates. They aren’t just checking your ID; they’re auditing your ‘reason to exist’ within the local market. Since the introduction of federal corporate tax in 2023, banks have also become part of the tax enforcement ecosystem, ensuring that companies aren’t using the UAE as a shell without real activity.

Banks prioritize three main factors when assessing international owners:

- Source of Wealth: Clear evidence of how you earned your initial investment capital.

- Transaction Patterns: Anticipated monthly volumes and the geographic location of your clients and suppliers.

- Regulatory Alignment: Whether your home country is currently on any international monitoring lists.

The Economic Substance Requirement

Economic substance is the defining requirement of 2026. Banks now demand proof that your company actually operates within the UAE. It’s no longer enough to have a ‘paper’ company. Having a local address, even a flexi-desk in a reputable free zone, serves as a vital signal of legitimacy. If your business activity is ‘International Trading’ but you don’t have a local warehouse or a clear logistics plan for the region, your application will likely hit a wall. Your banking profile must mirror your license activity perfectly to pass the initial screening. They want to see that your business is contributing to the UAE’s GDP, which exceeded $500 billion in 2023.

The Resident vs. Non-Resident Gap

The financial barrier to entry is notably higher for those without local status. While a resident might open a startup account with a zero-balance requirement, non-residents often face minimum average monthly balances starting at AED 50,000; these can climb to AED 200,000 for premium tiers. You’ll also find that features like cheque books or credit facilities are often restricted. This is why many founders choose to secure a resident visa UAE first. Transitioning to resident status unlocks better terms, lower fees, and a much faster approval timeline. A non-resident should plan for eight to twelve weeks for approval, while a resident might be active in two.

The Mandatory Corporate Documentation Checklist

Securing a corporate account in 2026 requires more than just a stack of papers; it requires a perfectly curated dossier. Banks have moved away from “box-ticking” and now perform deep-dive structural audits. Your documentation is the foundation of your credibility. If there’s a single discrepancy between your trade license and your share certificates, the compliance department will likely issue a hard rejection. Understanding the uae business bank account requirements for non-residents starts with gathering these five pillars of corporate identity.

- Valid UAE Trade License: Whether you’re in a Free Zone or Mainland, this must be current. Banks check the activity codes against your actual business model.

- Memorandum and Articles of Association (MOA/AOA): This document outlines your company’s internal rules. It must be signed by all shareholders.

- Certificate of Incorporation: This is your official “birth certificate” for the business, confirming its registration date and jurisdiction.

- Board Resolution: A formal document from the shareholders specifically authorizing the opening of the account and nominating the authorized signatories.

- Corporate Structure Chart: For companies with parent entities or multiple layers, a visual chart showing every shareholder is now mandatory.

The regulatory environment, as detailed in the UAE Investment Climate report, emphasizes transparency in foreign ownership. This means your paperwork must be beyond reproach. If your company is owned by another foreign entity, the bank will demand the full “pedigree” of that parent company too. Missing a single stamp can set your application back by four weeks or more.

Attestation and Legalization Rules

If your parent company is registered outside the UAE, your documents must be legalized. This usually involves a three-step process: notarization in the home country, attestation by that country’s Ministry of Foreign Affairs, and finally, attestation by the UAE Embassy there. Once the documents arrive in the UAE, they must be cleared by the local Ministry of Foreign Affairs (MOFA). If your documents aren’t in English or Arabic, you’ll need a legally certified translation. Most UAE banks accept English, but certain Mainland jurisdictions might require Arabic versions for their records.

Identifying Ultimate Beneficial Owners (UBO)

Transparency is the gold standard for 2026. You must complete a UBO Declaration form for any individual holding 25% or more of the company’s shares. Banks want to see through the corporate layers to the actual human beings who benefit from the profits. If you’re using nominee shareholders, be prepared for extreme scrutiny. The bank will want to see the underlying trust agreements or power of attorney documents. Providing a clear, honest picture of your ownership structure at the start is the fastest way to build trust with your relationship manager. If you’re feeling overwhelmed by these technicalities, our team can provide corporate bank account opening assistance to ensure your file is audit-ready before it reaches the bank.

Personal and Financial Proof for Shareholders

The bank’s compliance team doesn’t just look at your company’s potential; they look at your personal history and financial footprint. If you’re an international investor, you are the face of the business risk. Meeting the personal uae business bank account requirements for non-residents involves proving that you’re a low-risk, high-credibility partner with a transparent financial background. Banks in 2026 are particularly wary of “ghost owners,” so they require a comprehensive set of personal documents to verify your identity and your current place of residence.

- Passport Copies: You must provide high-resolution copies of your passport. Crucially, this must include the page with your most recent UAE entry stamp, even if you only visited as a tourist. This proves you’ve physically been in the country.

- Proof of Residence: You’ll need an original utility bill (water, electricity, or gas) or a bank statement from your home country. It must be less than 90 days old. A common mistake is providing a mobile phone bill or a document from a non-utility provider, which banks will reject immediately.

- Personal Bank Statements: Expect to provide at least six months of personal bank statements. These should show a consistent balance and clear transaction history.

- Professional Background: A detailed CV or an updated LinkedIn profile is now a standard requirement. Your professional experience must logically align with your new UAE business activity.

Proving Your Source of Wealth

Proving your Source of Wealth (SOW) is the most critical hurdle for non-residents. When reviewing UAE business banking requirements, you’ll find that the burden of proof lies entirely on the applicant. If you’re investing AED 100,000 into your new company, the bank wants to see exactly where that money came from. Acceptable proof includes three to six months of salary slips, audited financial statements from another business you own, or legal documents from a property sale or inheritance. If you can’t show a clear paper trail of your capital, the bank will likely flag the application for further investigation, leading to significant delays.

Business Plan and Projections

Your business plan isn’t just a marketing tool; it’s a risk assessment document. Banks require a 12-month cash flow projection that details your expected revenue and expenses. You’ll need to list your top five expected suppliers and customers, specifying whether they are local UAE entities or international firms. If your license is for “General Trading,” be prepared for intense scrutiny. Because this activity is so broad, banks view it as a higher risk for money laundering. Providing a specific, narrow business plan that explains exactly what you’re trading and with whom is the best way to satisfy uae business bank account requirements for non-residents in a high-compliance environment.

The Step-by-Step Application Roadmap for 2026

Applying for an account isn’t the first step; it’s the culmination of your formation strategy. If you’ve already incorporated without considering uae business bank account requirements for non-residents, you might find your specific license isn’t supported by your preferred bank. Successful applicants in 2026 follow a deliberate, phased approach that prioritizes compliance before submission. This roadmap ensures you don’t burn bridges with financial institutions by submitting a weak or incomplete file.

First, you’ll undergo a “soft review.” This is where you present your corporate profile to a relationship manager for an informal assessment. It’s a critical filter that prevents you from wasting weeks on a bank that doesn’t appetite your industry or turnover volume. If you get the green light, you’ll move to the documentation submission phase. This is the point where every signature must match and every stamp must be in place. Any discrepancy here triggers a “return to sender,” which can reset your timeline by 21 days.

Next comes the physical interview. Contrary to common misconceptions, most traditional UAE banks still require the authorized signatory to be physically present in the branch to sign the account opening forms and verify their original passport. Plan for a 48-hour trip to the UAE to finalize this step. Once signed, your file enters the compliance review, a 4-8 week period where background checks are finalized. Only after this deep dive will you receive your IBAN and instructions for the initial deposit to activate the account.

Choosing the Right Banking Partner

In 2026, the choice between digital and traditional depends on your transaction needs. Digital-first options like Wio or Mashreq Neo Business are often more accessible for startups, offering zero-balance structures for the first year. Conversely, traditional giants like Emirates NBD offer packages like the “Connect” account, which features a AED 0 minimum balance for a monthly fee of AED 249. If you require more robust features, ADCB’s SmartStart account charges AED 125 plus VAT monthly without a minimum balance. Always check if your chosen Free Zone has a pre-approved partnership with a specific bank, as this can shave meaningfully off your onboarding time.

Preparing for the Compliance Interview

The relationship manager isn’t just a salesperson; they’re the first line of defense. You’ll likely face questions about your “International Transactions,” specifically which countries you’ll send money to and receive it from. If you’re dealing with jurisdictions on international monitoring lists, your application will be rejected instantly. Be precise. Instead of saying “global trading,” specify that you’re “exporting textiles from India to the GCC.” Vague answers are the biggest red flag in 2026. If you want to ensure your profile is bulletproof before the meeting, our team provides corporate bank account opening assistance to guide you through every potential question.

Expert Corporate Bank Account Opening Assistance

Managing the uae business bank account requirements for non-residents is a full-time job that requires an insider’s perspective. You shouldn’t have to navigate these bureaucratic waters alone. At UAE Free Zone Finder, we act as the essential bridge between your international vision and the UAE’s strict financial gates. We don’t just provide a list of banks; we perform a comprehensive pre-screening of your entire dossier to identify the compliance traps that lead to the high rejection rates mentioned earlier. By the time your file reaches a relationship manager, it’s already been audited against the latest 2026 Central Bank protocols.

Our process begins with strategic alignment. We match your specific license type and business activity with the banks most likely to approve your profile. Some institutions prioritize tech startups, while others focus on high-turnover trading firms. By integrating your banking needs directly with your free zone company formation strategy, we ensure you aren’t stuck with a legal entity that local banks find difficult to onboard. We’ve seen many founders incorporate first and ask questions later, only to find their chosen jurisdiction isn’t on a bank’s “approved list” for non-residents.

Why a Strategic Setup Matters

Choosing the wrong jurisdiction can kill your banking chances before you even apply. If your business activity requires high-volume international transfers, certain offshore zones might be flagged as higher risk compared to a premier free zone with high economic substance. Utilizing professional corporate bank account opening assistance means you’re getting real-time intelligence on current bank appetites, which can shift monthly. We also provide ongoing support, helping you navigate the annual KYC updates that are now mandatory for all non-resident accounts to remain active and compliant.

Start Your UAE Journey Today

Don’t let the fear of complex uae business bank account requirements for non-residents stall your global expansion. We’ve helped thousands of entrepreneurs successfully navigate these hurdles with a focus on transparency and speed. We offer customized checklists based on your specific industry and expected turnover, ensuring no detail is overlooked. Take the first step toward your financial independence in the Middle East by speaking with a dedicated partner who knows the shortcuts. Speak with our banking experts now for a free consultation and a personalized roadmap to your company’s success.

Secure Your Global Business Future Today

Navigating the financial landscape of the Emirates in 2026 requires more than just a trade license; it demands a commitment to transparency and meticulous preparation. You’ve learned that documentation precision and a clear “Economic Substance” profile are the dual keys to unlocking the UAE’s banking sector. While the uae business bank account requirements for non-residents have evolved toward higher compliance, these hurdles are easily cleared when you have an insider guiding your application. Flawless execution during your physical interview and UBO disclosure will transform a “high-risk” label into a successful partnership.

As an UAE Free Zone Finder advisory team with 15+ years of UAE market expertise, we maintain direct relationships with leading UAE banks to ensure your file bypasses the common pitfalls. We don’t just help you open an account; we help you build a sustainable financial foundation for your international enterprise. It’s time to stop worrying about rejection letters and start focusing on your expansion. Get Expert Help with Your UAE Business Bank Account and let our specialists handle the bureaucracy. Your journey toward a seamless corporate banking experience begins with a single, strategic step.

Frequently Asked Questions

Can a non-resident open a business bank account in the UAE without a visa?

Yes, you can open a corporate account as a non-resident without a residency visa, but your options are more limited. Banks will classify you as an international investor, which usually means you won’t have access to cheque books or credit facilities. You’ll also face a much higher level of scrutiny regarding your global “Source of Wealth” and must provide a valid entry stamp in your passport to prove you’ve physically visited the country.

How much is the minimum balance for a non-resident business account?

Minimum balance requirements in 2026 range from AED 0 to AED 200,000 depending on the bank and package. Digital-first banks like Wio or RAKBank’s RAKstarter offer zero-balance accounts for the first 12 months. However, traditional institutions like Emirates NBD often require a minimum average monthly balance of AED 50,000 for their standard corporate packages. Failing to maintain these balances typically triggers a monthly penalty fee of approximately AED 150.

How long does it take to open a corporate account for a non-resident?

The approval process for non-residents typically takes between 8 and 12 weeks. This timeline is significantly longer than the 2-week average for residents because compliance departments must conduct international background checks and verify foreign documents. Providing a perfectly curated dossier at the start is the only way to avoid additional “Request for Information” (RFI) cycles that can push the timeline past the three-month mark.

Do I need to be physically present in the UAE to open the account?

Yes, the authorized signatory must be physically present in the UAE to finalize the application. While you can initiate the process and upload documents remotely, Central Bank regulations require a face-to-face meeting with a bank representative to verify your original passport. Most entrepreneurs plan a 48-hour trip to Dubai or Abu Dhabi specifically to sign the final bank forms and complete the mandatory KYC interview.

Which UAE banks are the most non-resident friendly in 2026?

Digital-first banks and specialized startup divisions are currently the most accessible for international owners. Wio Bank and Mashreq Neo Business have streamlined their onboarding for non-residents, often offering faster approvals through their mobile platforms. Among traditional banks, ADCB’s SmartStart and RAKBank’s RAKstarter remain popular choices due to their lower entry barriers and willingness to work with newly incorporated free zone entities.

What are the main reasons for non-resident bank account rejections?

Rejections are usually caused by a lack of “Economic Substance” or an unclear “Source of Wealth.” If you can’t provide a 3-month paper trail for your investment capital or if your business plan is too vague, the compliance team will flag you as high-risk. Additionally, choosing a “General Trading” license without a physical office or warehouse is a frequent trigger for immediate rejection in the 2026 regulatory environment.

Can I open a UAE business account online as a non-resident?

You can initiate the uae business bank account requirements for non-residents through digital apps, but a physical meeting is still required to activate the account. Platforms like Wio allow you to submit your trade license and passport copies digitally to start the screening process. However, you’ll still need to meet a bank officer in person within the UAE to perform the final identity verification before your IBAN becomes fully operational.

Is a physical office required for a non-resident business bank account?

Yes, having a physical address is now a non-negotiable requirement for most UAE banks. While a “flexi-desk” or “shared office” within a reputable free zone is often sufficient for consultancy or service-based startups, purely virtual setups are frequently rejected. Banks need to see that your business has a physical footprint in the country to satisfy 2026 Anti-Money Laundering (AML) and Economic Substance Regulations.

Disclaimer

The information provided in this article is intended for general informational purposes only and reflects conditions as understood at the time of publication. Free zone regulations, fees, and requirements in the UAE are subject to change. Readers are advised to verify details with the relevant free zone authority or regulatory body before making any business decisions. For personalised guidance, our business setup experts at UAE Free Zone Finder are available to assist — contact us at info@uaefreezonefinder.com or call +971-507864823.